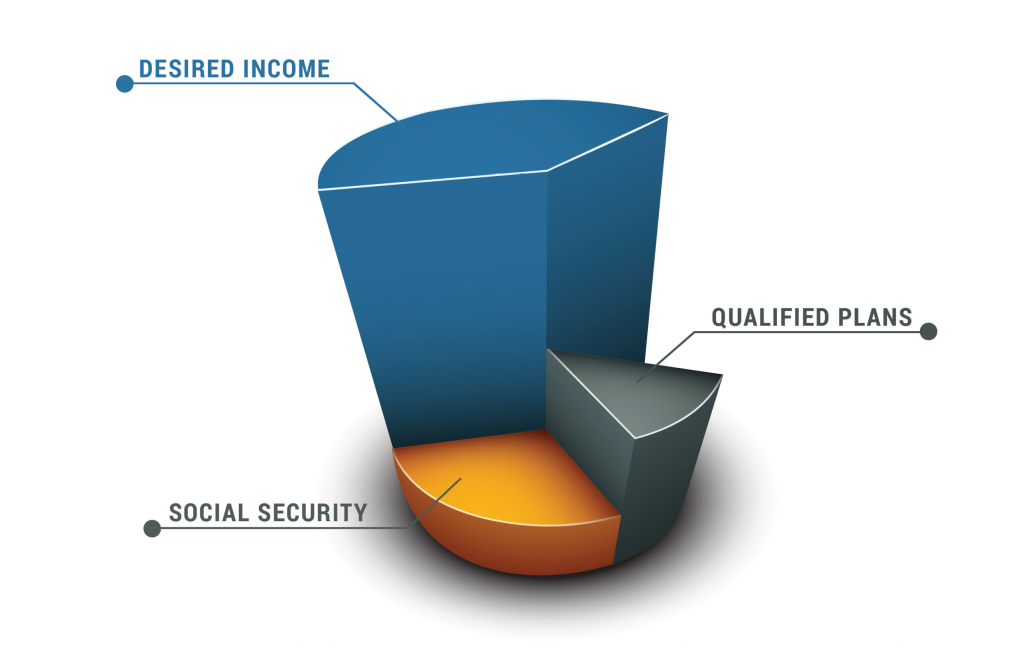

The Retirement Gap

Over the years, you've achieved a level of success few ever realize. But as your income has grown, your retirement investment options may have become more limited. You may face strict contribution limits on qualified plans or are excluded from some common plans such as Roth IRAs, making it difficult to meet you accumulation goals.

Your financial independence should reflect the level of success you've achieved. But without a strategy that seeks to enhance opportunities for tax-advantaged assets, you may be facing a significant future income gap. That gap could mean less freedom and security for your family, putting your financial strategy in jeopardy.

Thankfully, there's a solution.